My goal in this market report is to bring certainty in understanding our Somerset County real estate market through my expertise. My monthly market update walks you through the economic conditions and trends that influence our local markets. It also offers hyper-local statistics that you will not be able to find elsewhere. You will come away knowing not only “what” is happening in those markets, but more importantly, “why” is it happening. As a result, you will keep informed to make home buying and selling decisions in 2022.

“What’s” Happening in Somerset County’s Real Estate Market?

The buyers moving west from the New Your City area along with their higher wages have diminished greatly. As a result, we are starting to experience a significant slowdown as we are not seeing as many offers over asking as we did just a few months ago. Newly listed inventory has been up over the last month while showings and sales both are down. Home prices and interest rates are also both up, bringing buying power down. How do you make sense of it all? You will find the answer here.

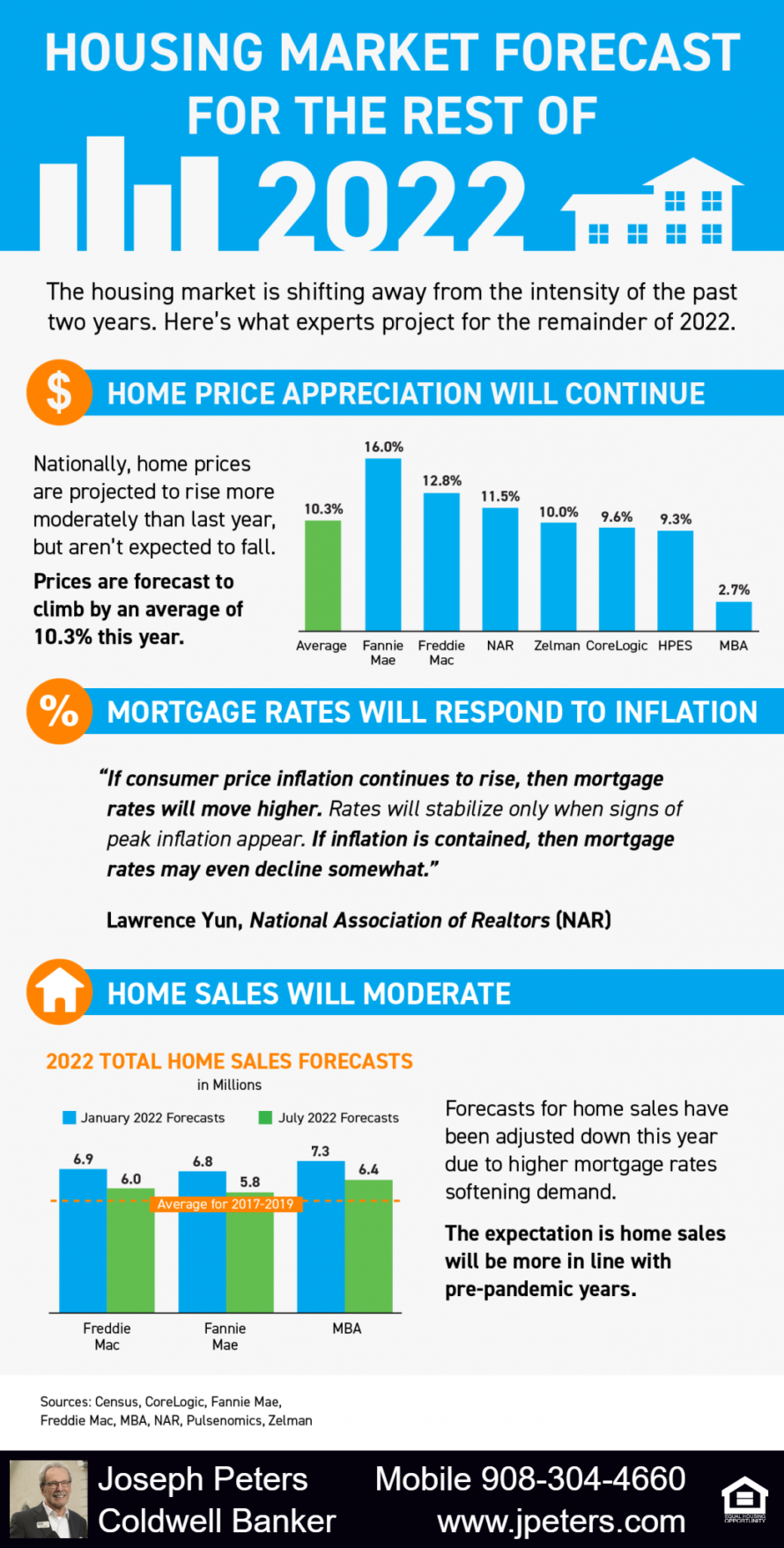

Still, fast-moving inventory and rising interest rates have resulted in a strong seller’s market keeping home prices on the rise (just not rising as quickly as in the recent past). We saw a nearly 20% rise in prices in 2021 and 12% in 2020. Although further increases will persist, we expect the rate of increase to diminish in 2022 but still see a possible 10 % appreciation in 2022. On the opposite side of the spectrum, the cost to own has risen from an average of 24% of gross income a year ago to over 30% today. This has knocked many first-time buyers out of the market. If you will be selling in 2022, waiting for later in the year is not a good strategy. The market is at its strongest now!

Contract sales decreased month over month in Somerset County in July by 56 units.

Based on the last month of contract sales (down 24% from the previous year), statistics show a fast-moving supply of inventory of just 1.8 months countywide. The units going under contract rose slightly to 26 days on the market. Three hundred and ninty-five units went “under contract” in July, down from 451 in the prior month. Newly listed properties in the same period totaled only 346 down from 433 in the preceding month.

Our inventory decreased from 715 this time last year to 701 units (2% less) due to the mentioned fast-moving market. But the inventory numbers were up 34 units in Somerset County vs. the prior month (a good sign for buyers).

Our sales decreased from 521 this time last year to 395 units (24% less). Sales were down 56 units over the prior month. We did see a slowing of first-time buyer activity (or their ability in finding affordable inventory). While many of the first-time buyers are being priced out of the market due to price + interest increases, it is still an optimum supply and demand curve for our sellers.

New Jersey Residential Real Estate Market Forecast

Because of the increased slowing move to the west (urban flight), pent-up demand, still relatively low (but rising) mortgage rates, and sellers coming on the market as Covid fears seem to be diminishing, we expect solid listings and sales thru the summer season. Just, not as strong as in 2021.

As previously mentioned, the new listings are selling fast. So, even though we still have low (but rising) inventory levels, sales are very strong. In 2021 we witnessed many homeowners facing financial and/or life uncertainty and holding off on listing their properties. In 2022, their biggest uncertainty is finding another more suitable house and a mortgage at an affordable price.

On the buyer side, it is estimated that the buyer of a median-priced house will need to earn $20 to 30K more than just a year ago in order to qualify for a mortgage as their mortgage as a percent of their income has risen. This is pricing many first-time buyers out of the market.

We are actually seeing fewer open houses and attendees in 2022 due to the fast pace of sales.

Somerset County Real Estate Market Inventory Breakdown By Price For Last Month:

| July | July | Total | ||

| Somerset County | New | Under | Active | Months’ |

| Listings | Contract | Listings | Supply | |

| Condos/Town Houses * | 105 | 148 | 171 | 1 |

| Over 55 Communities* | 11 | 15 | 31 | 2 |

| $000K to $199K | 4 | 9 | 14 | 4 |

| $200K to $299K | 22 | 38 | 40 | 2 |

| $300K to $399K | 85 | 99 | 139 | 2 |

| $400K to $499K | 55 | 60 | 99 | 2 |

| $500K to $599K | 37 | 46 | 67 | 2 |

| $600K to $699K | 33 | 40 | 61 | 2 |

| $700K to $799K | 29 | 30 | 56 | 2 |

| $800K to $899K | 19 | 20 | 33 | 2 |

| $900K to $999K | 14 | 15 | 29 | 2 |

| $1,000K and Up | 48 | 38 | 163 | 3 |

| Totals for July | 346 | 395 | 701 | 2 |

| Average Price | $708,804 | $610,532 | -13.9% | |

| Average Days on Market | 26 | |||

| * Included in $ breakdowns |

- 52% of sales in houses > $500,000

- 38% of sales in the $500,000 to $1,000,00K range

- 10% percent of total sales (or 41 in total) in houses >$1,000,000

Somerset County Real Estate Market Inventory Breakdown By Municipality For Last Month:

| Active Listings | Under Contract | Month’s Supply | |

| Bedminster Twp | 40 | 23 | 2 |

| Bernards Twp | 59 | 37 | 2 |

| Bernardsville | 32 | 14 | 2 |

| Bound Brook | 16 | 10 | 2 |

| Branchburg Twp | 26 | 16 | 2 |

| Bridgewater Twp | 68 | 45 | 2 |

| Far Hills Boro | 5 | 0 | |

| Franklin Twp | 97 | 71 | 1 |

| Green Brook | 29 | 11 | 3 |

| Hillsborough | 66 | 56 | 1 |

| Manville Boro | 29 | 14 | 2 |

| Millstone Boro | 1 | 2 | 1 |

| Montgomery Twp | 48 | 20 | 2 |

| North Plainfield | 26 | 15 | 2 |

| Peapack Gladstone | 6 | 0 | |

| Raritan Boro | 8 | 8 | 1 |

| Rocky Hill Boro | 1 | 0 | |

| Somerville Boro | 30 | 10 | 3 |

| South Bound Brook | 14 | 4 | 4 |

| Warren Twp | 73 | 26 | 3 |

| Watchung Boro | 27 | 13 | 2 |

| Totals | 701 | 395 | 2 |

One area had no sales last month:

- Far Hills

- Peapack/Gladstone

- Rocky Hill

One area reported 3 sales or less each last month:

- Millstone

Hotspots:

- Bernards/Bernards Twp. – 60 Sales

- Bridgewater – 45 Sales

- Franklin Twp. – 71 Sales

- Hillsborough – 56 Sales

- Warren/Watchung – 39 Sales

These hotspot areas equaled 68% of the sales last month. The average new listing coming on the market last month neared $708,804. The average unit price going “under contract” was $610,532 (14% less).

Bridgewater Township Statistics:

- There are 68 homes for sale in Bridgewater Township as of this writing.

- Of the 68 homes for sale, 13 are community properties (such as townhouses and condos) and two is in our 55+ communities

- The average list price for all listings in Bridgewater Township is $683,516.

- There were 39 new listings in Bridgewater Township last month with an average list price of $645,738.

- There were also 45 homes that have gone under contract in the past 30 days with an average list price of $535,354 and 23 days on market.

- Giving us about 1.6 month of inventory

- Call for additional details

Note: To get a competitive price point on your property based on location and uniqueness, contact me at (908) 304-4660. Coldwell Banker’s big data technology and Artificial intelligence capabilities will give you a unique advantage. I can show you the latest age and earnings breakdown for your particular area where people move from into that area and how I can directly market to those specific areas and demographics. The result is that you receive the maximum selling price with a shorter time on the market. Houses priced and marketed accurately sell faster, especially with a real estate industry veteran and local expert helping you navigate the process.

“Why” is it happening

New Jersey’s Economic Drivers:

New Jersey Home Sales and inventory levels:

- The rebound that started in June 2020 has continued through the Early Summer of 2022 is now slowing.

- We have seen signs of first-time buyers cooling down, mainly due to higher pricing, inventory shortages, and the rising interest rate factors pushing many of them out of the market.

- Many possible sellers are experiencing difficulty in finding other suitable housing themselves. They sort of get in their own way in not wanting to list until they find it. They also need to find affordable financing with mortgage rates being up.

- The current month’s supply of inventory in Hunterdon and Somerset County is now just under two months, and this is due to the extremely quick sales of new listings as they come on the market which is called velocity. The market does remain very active.

- Hunterdon and Somerset County have about 10% & 2% less inventory than we had a year ago, respectively. This picture has improved nicely over the last month in Somerset county but slipped just a bit in Hunterdon County. over the last month.

- Unsold inventory in N.J. has steadily increased state-wide since the beginning of the year adding nearly 8,000 homes to the market.

- Decreases in inventory have occurred in many price points, with the under $400,000 market seeing the most considerable impact with 12% fewer homes while the $400K to $600K is now showing the largest increase in inventory.

- New housing has simply not kept up with our population growth.

Interest Rates:

- Interest rates have held steady over the past few weeks but are threatening to inch up even further.

- The economy is adjusting, and average Interest rates are holding for now 5.3% for a 30-year conventional mortgage. A fifteen-year conventional mortgage rests at the 4.6% mark, and five-year arms are under the 4.3% range.

- As said, rates in the last few months have been inching up based on the 10-year note yield. For the past couple of months, consumer prices (inflation) have run above the 30-year mortgage rates for the first time in 50 years. As this is unsustainable, either we will need to see inflation come down a lot, mortgage rates rise, or both.

- Also, we are now seeing additional activity to ease (or temper) the amount of mortgage-backed securities that the Fed buys each month, which will negatively affect rates going forward. In effect, the rates have already inched up a bit due to this.

- Based on the rising rates, we are seeing a drop in first-time buyer mortgages, but are still active in restructuring debt and paying down high-interest items.

National Job Front:

- In the first quarter of 2022, the country added about 1.7 million jobs. This is about where this percentage was pre-pandemic. In June we added another 372,000 jobs. July numbers are not yet out.

- We have to keep in mind that we have natural job growth of about 175K per month which this number includes.

- In July, the unemployment rate edged down to 3.5 percent, and the number of unemployed persons edged down to 5.7 million. These measures have returned to their levels in February 2020, prior to the coronavirus (COVID-19) pandemic.

- The labor force participation rate, at 62.1 percent, and the employment-population ratio, at 60.0 percent, were little changed over the month. Both measures remain below their February 2020 values (63.4 percent and 61.2 percent, respectively)

- Also, we are seeing many resignations as the workforce repurposes itself. These are due to people switching careers due to the desire to pursue new career paths, perceived health risks in their current jobs, the desire for more remote work, and better work-life balance. New technology-based jobs are now affecting this trend.

- In the under $50K earners, there is even some incentive not to work and collect benefits for an advantage over wages.

- And, as a result, we currently have about 5.9 million unemployed, while there are an estimated 12 million job openings at this point. That is two jobs available for every job seeker driving wages up.

- The lower end of the job market has benefited the most from this phenomenon as we see higher starting pay rates competing for the lack of workforce. We are already seeing jobs starting in the mid to upper $20 per hour ranges being offered.

New Jersey Job Front:

- The NJ unemployment numbers are still higher than the U.S. at 3.9% for the last month reported which was may. NJ has now recovered about 98% of the jobs lost in the initial months of the pandemic.

- Construction, food services, and accommodations are again the leaders in job losses, though more states are now citing pain in retail and wholesale trade. Health care, social assistance, and manufacturing are shedding workers, too.

- N.J. was hit early and hard by the pandemic with almost twice the national rate of job losses. So, where it is currently is quite remarkable.

- But, the job losses will undoubtedly impact the lower end of the buyer’s market in 2022.

Rental Market Trends:

- Rental prices in New Jersey rose again through 2021, averaging 8+% higher year-over-year, and are averaging just over $2,000 per unit.

- The central N.J. vacancy rate now stands at 2.6 resulting which is a minimal rental supply.

- The rental market sector usually reflects some low-end buyers now renting due to inventory constraints. This sector has now risen due to mortgage constraints as well.

New Jersey Foreclosures:

- This is a bright spot for NJ.

- The delinquency rate in NJ has decreased again.

- Current foreclosures in NJ are at 1.9% which is good news.

- On a national basis there is sufficient equity ($11 Trillion) to protect most homeowners should we encounter a recesion (which seems inevitable).

- And, we have an average FICO score of mortgage holders of over 750 vs. the under 700 number we saw with the last bust in 2008.

- Yet, a recession could cost jobs and put more mortgages at risk in the future.

- Only 300K mortgages are at risk nationwide due to forbearance issues not being resolved. So, a housing bust is not predicted to be anywhere on the horizon.

- However, this effect will be nowhere near the last housing crisis since the is a lot of positive equity in houses today as many homeowners have more equity due to the past several years appreciations.

Real Estate Market Recap

Changes in Lifestyle (Non-Covid):

- The average age at marriage has risen to the mid-thirties.

- Due to costs and the ability to choose, families usually have only one (or maybe two) children. The national births per woman is now nearing 1.5 children per family, while the number needed to maintain our current population level is 2.1. If this continues, the result will be a fore-coming population implosion.

- And, the fact that people are living longer helps support the workforce with many seniors still in the job market.

- In many job markets, immigration is now also supplementing and supporting the workforce numbers.

- As a result of prior job opportunities, buyers once gravitated to areas within 15 miles of NYC with sound mass transportation systems.

- Starting several years ago, we were beginning to see a reversal of the above as late millennials were looking for more space and a place to raise their upcoming families better.

- This trend was sure to continue as 80% of consumers still perceive homeownership as part of the American Dream. It is just what they want to buy (or rent) that has changed.

- Builders have built most of the affordable land. Affordability is affected by local zoning, safety, and environmental constraints.

- While first-time buyers are typically looking for smaller sub $400K single-family or luxury hi-rise properties, builders target much larger and more costly projects in scope or rentals.

- 70% of all NJ homes have no children of school age, and 50% do not have more than one person in them, and this factor minimizes the need for larger housing.

- The majority of all new housing starts in 2021 in NJ were in the rental sector, and the 2022 numbers look to surpass that contributing to the lack of new construction and inventory.

- Also, builders are encountering severe supply chain issues causing delays and erratic increases in pricing.

- The recent trend of moving further away from the city to more rural areas which was helping Hunterdon and Somerset counties has now slowed.

- We are also seeing the formation of multi-generational housing due to the difficulty in finding new housing.

- And, we could see additional work-from-home job opportunities as we see more emerging/disruptive advances in technology which allows this westward move to happen.

- In effect, Covid-19 has caused the speed of the evolution of these technologies to increase.

Changes in Lifestyle (Covid Related):

- The “Great American Move” to more rural areas is a term that we are starting to see for this new lifestyle exacerbated by the pandemic and civil unrest in metropolitan cities.

- Many workers now only have to go to the office only on occasion, allowing them to live further out in the “burbs”. And, they were bringing their NYC salaries with them helping to drive up prices.

- But, this move is primarily among the more educated and skilled workers that can use technology to adapt to a work-from-home environment.

- Many professionals such as medical and first responders as well as many lower-skilled/educated service sector workers cannot work remotely from home.

- There is an open question of how many workers will continue to gravitate away from (or return to) the city as they adapt to work from home environments and as buyers need a live/work/play/learn environment. This trend already seems to have slowed greatly.

- Many people have rethought their lifestyles, and are changing jobs and work locations to accommodate their new thinking.

- Also, workers can now find more competitive wages in the lower end of this job market, allowing them to consider more rural options.

- Open floor plans, the list-topper for the past twenty years, seem no longer important as buyers gravitated towards more compartmentalization within the home.

- Live/Work/Education/Exercise (or play) areas are now vital.

- Smart home technologies are now in.

- Also, backyard recreation facilities such as recreational areas and pools are now preferred, and backyard oasis environments add value to the above lifestyle.

- There is also an interest in properties with outbuildings and studios/Lofts.

Market conditions:

- What a difference we have seen in consumer thinking since the pandemic started. And it is still evolving and to some extent changing back.

- Consumer confidence was put on pause in early 2020 and then started to fast forward in June of 2020 and did not slow appreciably until early 2022. But now, with talks of recession, this too has reversed itself. Consumer confidence has plummeted to a 7o year low.

- This can accelerate a recession, as it will mean, less spending, fewer sales, fewer jobs, and higher unemployment. None of this helps the housing market.

- We are already seeing a slowdown with fewer people moving westward, fewer home sales, less multiple bid situations. Our local housing inventor is rising as a result. And, with just under two months’ supply, it is still a seller’s market.

- Consumers still see homeownership as a sound long-term investment based on affordability. It is just that their shopping list as to what they want has changed.

- And, in general, homeowners are sitting with more equity than ever (NJ reports 95+% with positive equity) and are no longer using their homes as an ATM. The average equity in NJ rose by $55K over the past year due to price increases.

- In 2021/22, many strong equity homeowners will decide to sell or trade to take advantage of the buying surge as they rethink their housing options.

- Some moved to their second homes or out of state as they no longer needed to commute.

- Others pushed up their retirement plans.

- The current seller’s market has resulted as we still have many more buyers than sellers (which results in rising home values).

- People usually buy and sell homes based on life events and will not change. Life events have gone on (sometimes even moving faster).

- And never before seen (but now steadily rising) low-interest rates plus the move west has helped the migration pattern towards NYC reverse.

- We are seeing a continued downtrend in new cases as the vaccines are starting to become a reality and things are better understood, and people get back to a new normal lifestyle.

- The new virus variants now seem to be diminishing.

- But it is anticipated that the new lifestyle will be much different from the old as we adopt the best of the two cultures.

- Nation-wide we sold more houses in 2021 than in 2020. And 2022 was seen as even robust but is now being threatened.

- The current shortage is for a different reason than in 2021. People who want to list their homes in 2021 are now hesitant due to finding new housing and financing themselves. The problem is feeding on itself.

- As a result, we see many offers with competitive terms like waiving appraisals and inspections.

- Because of the above point, we are now starting to see a lot of buyer fatigue in the under $400K market as first-time buyers are getting priced out of the market.

- In Hunterdon and Somerset counties, the buyer of an average-priced house now needs to earn about 25% more just to qualify for what they were able to buy just a year ago.

- But, we anticipate an active but less hectic late summer and early fall season in 2022. It really looks like we are headed back to more normal pre-pandemic market conditions.

Forecast:

- The effect of the COVID-19 pandemic now seems to be almost under control (let’s hope).

- The economy is recovering (but at a slower pace) from the recent cooling in employment numbers.

- Supply chain shortages have been affecting inflation. There are even now some concerns that we may are oversupplied and this could suddenly reverse causing massive price reductions and possible lay-offs.

- Inflation is continuing to cause havoc on auto, finished goods, and energy pricing.

- The recent invasion of Europe has shed some doubt on market predictability. In effect, we have never seen a pandemic followed by a war. The near future is somewhat unpredictable.

- Mortgage rates continue to slowly rise and are now at 5.8% as the fed is tapering its current level of investment in mortgage-backed securities. It looks like this is certain to rise further.

- Inventory supply continues to increase in the above $400K market as we move further into 2022.

- The housing affordability index is better than ever, with mortgage payments nearing 30% of gross.

- But, we are starting to see the consumer sentiment index wain due to inflation and that is concerning.

- Due to the COVID-19 and recent unrest in NYC, we were starting to see more interest in living in more suburban counties such as Hunterdon and Somerset. That has wained somewhat.

- Also, many people have found that working from home (either in total or part) is a reality, and we will see less commuting and traveling in general as things start to open up once again.

- What were once “bedroom” communities are changing to” live, work, play & learn” communities bringing lots of change to our local economies.

- It is only a matter of time before we see more jobs (or remote capabilities) following workers into our suburban areas.

- Retailing and using vacant industrial space will transform to meet the new altered demands and lifestyles.

- More attention is now given to houses with pools and backyard spas and less open areas which lend themselves to working and studying at home.

- And, the local market will have to adapt to the new suburban renaissance of where people will be working from and what they will need to adapt to this.

- The lingering question is, “Can we keep this momentum up with low to falling inventory?”. Even with last month’s increases, predictions are for slower sales and price increases in the balance of 2022.

- Also, what will be the effect of continued inflation on the economy? It is already affecting mortgage rates. And retail sales are not advancing faster than inflation. This is very concerning.

- Job opportunities will surely follow the workforce and housing then follow jobs. It seems out of logical sequence but will sort itself out as we progress.

- Depending on their location and price points, local property values saw at least 18%+ appreciation in 2021 and another 12% in 2020. The 2022 appreciation forecast is looking as they will be around 9%.

- Days on the market in our area are holding steady showing active buyers.

- But this could change back towards a more normalized environment if inventory continues coming on to the market and the buyer fatigue that we have seen continues.

- We still have many younger (millennial) buyers coming of age in the pipeline for at least the next four to five years, which will continue to put more demand on the first-time buyer market, usually under $400K.

Futures:

- Remote work demands have caused technology t0 to evolve quickly and offer many new options in the Live/Work/Plan/Learn environments. Areas to watch are:

- Virtual Reality (a form of VR is where you can virtually walk thru a house while sitting at your PC or Tablet (see example)

- Augmented Reality (where you can place a piece of furniture in a 3D rendering of a room in your home or try on glasses, makeup, or clothes)

- Artificial Intelligence (which will utilize computer analysis of data to help make decisions). I use this to understand where buyers are moving from to an area and then advertise when listing a new house to those zip codes (see short video).

- Robotics (we see this today via vacumes, lawnmowers, and pool cleaners). Drone usage is another good example.

- The Internet of Things (IOT) is allowing us to connect more and more things to our smart homes.

- Increased 5G availability (having the speed to do more things remotely)

- 3D printing (having the ability to deliver an item remotely)

- Autonomous driving (eliminating the need for delivery drivers, for example)

- As the demand for remote capabilities increases, these technologies will meet the challenges, and the convergences of several of them will offer capabilities that we have never even envisioned in the past.

- They will also eliminate many jobs as we know them today. One estimate states that 80% of all jobs we currently know will disappear over the next ten years and be replaced (in part) by new occupations (many of them being remote).

- Resulting unemployment will require retraining and repurposing many employees.

All of this has been taking place in the past. But the requirement for remote capabilities and lack of workforce has significantly sped up their development cycle. In essence, we have pushed 5 years of advancement in these technologies into the past year. And, it looks like it will continue.

Wow. That is a lot to digest. And it is changing daily but seems to be heading in the right direction for now. For clarity and understanding, I am always available if you want to talk and better understand how this might affect your particular situation. You can contact me at (908) 304-4660.

Note: Presented as a public service by Joe Peters of Coldwell Banker Residential Brokerage. I took reasonable precautions in presenting this information. Please consult with a professional sales agent and take no actions based on my opinions, gathered trends, and statistics. I assume no liability.

You can ask me a question or request a monthly copy of this newsletter here.